Aapne saalon tak premium bhara. Har mahine, har saal, bina chuke. Jab zaroorat aayi — hospital mein admit hue, accident hua, ya family member ki death hui — tab claim kiya. Aur insurance company ne bola — “Sorry, aapka claim reject kiya jaata hai.”

Yeh sunke lagta hai jaise zameen paav ke neeche se khisak gayi. Lakho rupaye ka treatment hua, aur insurance claim reject ho gaya? Ab kya karein?

Pehli baat — ghabraane ki zaroorat nahi hai. Insurance company ka rejection final nahi hai. Aapke paas legal rights hain — aur India mein ek clear system hai jisse aap insurance claim reject hone ke baad bhi apna poora paisa wapas le sakte hain.

Main ek practicing advocate hoon aur maine personally aise cases handle kiye hain jahan insurance claim reject hone ke baad clients ko lakho rupaye ka compensation mila — interest ke saath. Consumer court ne insurance companies ko Rs 50 lakh+ ka payment karne ka order diya hai bahut se cases mein.

Is article mein main aapko bataunga — insurance claim reject kyun hota hai, kya karna chahiye turant, complaint kahan karni hai (4-tier system), kaunse documents chahiye, kitna time lagta hai, aur kaise apna paisa wapas lein.

Quick Answer: Insurance claim reject hone pe — (1) rejection letter carefully padhein aur reason samjhein, (2) insurance company ke Grievance Redressal Officer (GRO) ko written appeal karo, (3) 15 din mein response na aaye toh IRDAI ke Bima Bharosa portal pe complaint karo, (4) Ombudsman ke paas jaao (Rs 50 lakh tak, free, binding order), (5) satisfy nahi toh Consumer Court mein case karo. 8 saal se zyada premium bhara hai toh Moratorium Rule ke under company claim deny nahi kar sakti.

Also Read:- Cyber Crime Complaint Kaise Kare 2026 — Online FIR Aur Portal (Complete Guide)

Insurance Claim Reject Kyun Hota Hai — 10 Common Reasons

Pehle yeh samjhein ki insurance companies insurance claim reject kyun karti hain. Reasons jaanoge toh appeal strong banegi.

Health Insurance Mein Common Reasons:

1. Pre-existing disease declare nahi ki Sabse common reason. Aapne policy lete waqt koi bimari nahi bataayi (diabetes, BP, thyroid) aur baad mein usi se related treatment hua. Company kehti hai “non-disclosure.”

2. Waiting period complete nahi hua Bahut si bimariyon pe 2-4 saal ka waiting period hota hai (knee replacement, cataract, hernia). Waiting period mein claim kiya toh reject hoga.

3. Excluded treatment/procedure Policy mein kuch treatments covered nahi hote — cosmetic surgery, dental (unless accident), fertility treatment, etc.

4. Hospitalization zaroori nahi thi Company ka TPA (Third Party Administrator) kehta hai “yeh treatment OPD mein ho sakta tha, admission ki zaroorat nahi thi.”

5. Policy expired ya premium lapse Premium time pe nahi bhara — grace period bhi beet gayi — policy lapse ho gayi. Claim kiya toh reject.

Motor/Car Insurance Mein:

6. Drunk driving ya invalid license Accident ke waqt driver ke paas valid license nahi tha ya alcohol/drugs ke influence mein tha.

7. Wear and tear claim kiya Insurance sirf accident/damage cover karta hai — normal wear and tear, mechanical breakdown cover nahi hoti.

Life Insurance Mein:

8. Material fact suppress kiya Policy lete waqt smoking habit, alcohol consumption, ya koi serious illness nahi bataayi.

9. Suicide clause (1 saal ke andar) Zyaadatar life insurance policies mein pehle 1 saal ke andar suicide pe claim nahi milta.

10. Nominee dispute Multiple nominees mein dispute — company claim hold kare deti hai.

Advocate’s Note: Agar aapne 8 saal se zyada continuously premium bhara hai toh IRDAI ka Moratorium Rule lagta hai. Iske baad company pre-existing disease ke basis pe insurance claim reject nahi kar sakti — chahe aapne disclosure mein kuch chhupa bhi ho. Yeh 2024 se effective hai aur bahut powerful protection hai.

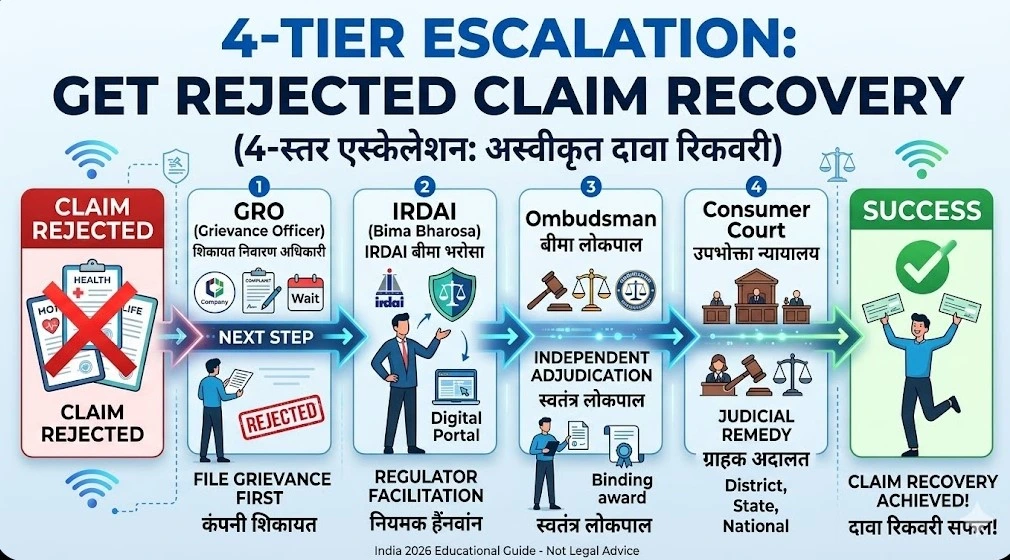

Insurance Claim Reject Hone Ke Baad Kya Kare — 4-Tier Recovery System

India mein ek clear 4-tier system hai insurance claim reject challenge karne ke liye. Har tier pe chances badhte hain.

Tier 1: Insurance Company Ka Grievance Redressal Officer (GRO)

Pehla step — hamesha yahi se shuru karo.

Har insurance company mein ek Grievance Redressal Officer (GRO) hota hai. IRDAI ke rules ke under yeh mandatory hai.

Kya karna hai:

- Rejection letter mein reason carefully padhein

- GRO ko written complaint bhejo — email + registered post dono se

- Complaint mein likho:

- Policy number

- Claim number

- Rejection ka reason (company ne kya bola)

- Aapka counter-argument (kyun rejection galat hai)

- Kaunse documents support karte hain aapki baat

- Kya relief chahiye (claim amount + interest)

- 15 days ka deadline hai company ke liye respond karne ka

Response possible outcomes:

- Company agree kar le — claim approve ho jaaye (best case)

- Company partially agree kare — kuch amount offer kare

- Company reject kare — tab next tier pe jaao

Tier 2: IRDAI Ka Bima Bharosa Portal

Agar company 15 din mein respond nahi karti ya unsatisfactory response deti:

Website: bimabharosa.irdai.gov.in

Step-by-step:

- Portal pe register karo

- “Register Complaint” pe click karo

- Policy details, insurer name, complaint nature bharo

- Rejection letter aur supporting documents upload karo

- Submit karo — complaint reference number save karo

Kya hota hai:

- IRDAI complaint insurer ko forward karti hai

- Insurer ko stipulated time mein respond karna hota hai

- IRDAI monitor karti hai progress

Alternate ways to reach IRDAI:

- Email: complaints@irdai.gov.in

- Toll-free: 155255 ya 1800 4254 732

- Post: General Manager, IRDAI, Hyderabad

Tier 3: Insurance Ombudsman (Sabse Effective — FREE)

Yeh sabse powerful tool hai insurance claim reject challenge karne ka.

Kya hai: Insurance Ombudsman ek quasi-judicial authority hai jo insurance disputes resolve karti hai — bilkul free mein.

Website: cioins.co.in

Eligibility:

- Aapne pehle company ko complaint ki ho aur woh resolve nahi hua (ya 30 din mein response nahi aaya)

- Claim amount Rs 50 lakh tak ho

- Complaint 1 saal ke andar honi chahiye rejection date se

- Same issue pe court ya consumer forum mein case pending nahi hona chahiye

Process:

- cioins.co.in pe jaao

- “Register Complaint” pe click karo

- Details bharo — policy, rejection, complaint history

- Documents upload karo

- Submit karo

Ombudsman ka power:

- Dono parties ko sun sakta hai

- Evidence examine kar sakta hai

- Binding award de sakta hai insurer pe (insurer ko maanna padega)

- Aap pe binding nahi hai — agar satisfy nahi hain toh consumer court ja sakte hain

- No fee — completely free process

- 3 months mein decision aana chahiye

Pro Tip: Ombudsman ka award insurer pe binding hai — yaani agar Ombudsman ne bola “claim pay karo” toh company ko karna padega. Lekin agar aap Ombudsman ke decision se satisfy nahi hain toh aap consumer court ja sakte hain. Yeh one-way binding hai — aapke favour mein.

Tier 4: Consumer Court (Last Resort — But Most Powerful)

Agar Ombudsman se bhi satisfy nahi hain ya claim Rs 50 lakh se zyada hai:

Kahan file karein:

- Rs 1 crore tak: District Consumer Forum (e-daakhil.nic.in se online file karo)

- Rs 1-10 crore: State Consumer Commission

- Rs 10 crore+: National Consumer Commission (NCDRC)

Ground: “Deficiency of service” — Consumer Protection Act, 2019 ke under

Consumer Court ka power:

- Claim amount pay karne ka order

- Interest award kar sakta hai (usually 9-12% per annum)

- Compensation de sakta hai mental harassment, inconvenience ke liye

- Litigation cost bhi insurer se dilwa sakta hai

- Penalty laga sakta hai unfair trade practice ke liye

Timeline: Simple cases 6-12 months, complex cases 1-2 saal.

Documents Jo Aapke Paas Ready Hone Chahiye

Insurance claim reject challenge karte waqt yeh documents zaroor rakhein — har stage pe chahiye honge:

- Policy document (original copy)

- Premium payment receipts (sab saalon ke)

- Claim form (jo aapne submit kiya tha)

- Rejection letter (insurance company ka — yeh sabse important document hai)

- Medical records (discharge summary, doctor’s prescription, test reports — health insurance mein)

- Hospital bills (itemized — OT charges, medicine, room rent sab alag)

- FIR copy (motor insurance mein — accident ke case mein)

- Repair estimates / bills (motor insurance mein)

- Death certificate (life insurance claim mein)

- Correspondence — company ke saath email, letters, calls ki recording

- GRO complaint copy aur response (agar mila toh)

- IRDAI complaint acknowledgement

Advocate’s Note: Rejection letter sabse important document hai. Iske bina appeal weak hogi. Agar company ne verbal reject kiya hai toh written rejection letter maango — yeh aapka legal right hai. Bina written rejection ke Ombudsman aur Consumer Court mein case difficult hota hai.

Real Case Study — Health Insurance Claim Rs 4.8 Lakh Ka Recovery

Background: Mrs. Verma (age 55), Gurugram. Unki health insurance policy thi — Rs 10 lakh cover, ek private insurer se. 6 saal se premium bhar rahi thi.

Problem: Mrs. Verma ko knee replacement surgery karwani padi. Total hospital bill: Rs 4,80,000. Company ne insurance claim reject kiya — reason: “Pre-existing condition — osteoarthritis was not disclosed at the time of policy inception.”

Mrs. Verma ka argument: “Mujhe osteoarthritis ka pata 3 saal pehle chala — policy lene ke baad. Maine koi bimari chhupaayi nahi thi.”

Action:

- GRO ko appeal likhi — medical records ke saath jo prove karte the ki diagnosis policy ke baad hua. Company ne 20 din mein reject kar diya.

- Bima Bharosa portal pe IRDAI complaint ki — company ne partial settlement offer kiya Rs 2 lakh ka. Mrs. Verma ne refuse kiya.

- Insurance Ombudsman ke paas gayi — dono sides ke documents dekhe, hearing hui.

Ombudsman ka decision:

- Company ka rejection unjustified hai

- Osteoarthritis ka diagnosis policy ke 3 saal baad hua — non-disclosure nahi hai

- Company ko Rs 4,80,000 full claim pay karna hoga + Rs 50,000 compensation for mental harassment

- Total: Rs 5,30,000

Timeline: GRO se Ombudsman decision tak — approximately 5 months.

Key Takeaway: Agar aapka insurance claim reject hua hai toh seedha accept mat karo. System use karo — GRO, IRDAI, Ombudsman. Bahut se cases mein company galat hoti hai.

Moratorium Rule — 8 Saal Ke Baad Company Claim Deny Nahi Kar Sakti

Yeh 2024 se effective hua hai aur bahut kam logo ko pata hai.

IRDAI ka Moratorium Rule:

- Agar aapne 8 saal continuously premium bhara hai (koi break nahi)

- Toh company pre-existing disease ke basis pe claim reject nahi kar sakti

- Chahe aapne policy lete waqt koi bimari chhupaayi bhi ho

- Sirf proven fraud ke case mein company deny kar sakti hai

Example: Aapne 2015 mein policy li. Diabetes nahi bataayi. 2023 mein (8 saal baad) diabetes related hospitalization hua. Company claim reject karti hai — “non-disclosure.” But Moratorium Rule ke under company galat hai — 8 saal ho gaye, ab deny nahi kar sakti.

Yeh rule insurance claim reject cases mein sabse strong defense hai agar aapki policy purani hai.

5 Myths — Insurance Claim Ke Baare Mein Galat Dhaaranayein

Myth 1: “Insurance company ne reject kiya toh ab kuch nahi ho sakta”

Sach: Bilkul galat. 4-tier system hai — GRO, IRDAI, Ombudsman, Consumer Court. Ombudsman ka process free hai aur binding order deta hai. Consumer court mein interest aur compensation bhi milta hai.

Myth 2: “Ombudsman ke paas jaane ke liye lawyer chahiye”

Sach: Nahi chahiye. Ombudsman process simple hai — aap khud represent kar sakte hain. No fee, no lawyer mandatory. Lekin complex cases mein advocate helpful hota hai.

Myth 3: “Consumer court mein case karna bahut mehenga aur time-consuming hai”

Sach: e-daakhil.nic.in se online file hota hai. Court fee nominal hai (claim amount ke basis pe). Simple insurance claim reject cases 6-12 months mein resolve hote hain. Advocate fee bhi insurer se dilwaya ja sakta hai agar aap jeette hain.

Myth 4: “Agar maine pre-existing disease nahi bataayi toh mera koi right nahi”

Sach: 8 saal ka Moratorium Rule lagta hai. 8 saal ke baad pre-existing disease ka excuse nahi chalega. Plus agar disease policy ke baad develop hui toh woh pre-existing hai hi nahi.

Myth 5: “Insurance claim sirf policyholder hi kar sakta hai”

Sach: Nominee, legal heir, assignee — sab claim kar sakte hain. Death claim mein nominee file karta hai. Agar nominee nahi hai toh legal heirs succession certificate ke saath claim kar sakte hain.

Insurance Claim Reject Se Bachne Ke 7 Tips

- Policy lete waqt sab kuch disclose karo — har bimari, har surgery, har medication. Chhupana sabse bada risk hai

- Proposal form khud padhke sign karo — agent pe blindly trust mat karo

- Policy document padhein — exclusions, waiting periods, sub-limits samjhein

- Premium time pe bharein — grace period ke andar. Lapse hone pe claim nahi milega

- Cashless network hospital mein treatment lo — reimbursement mein delays zyada hote hain

- Har document save rakhein — bills, prescriptions, discharge summary, test reports

- Claim form mein sab details sahi bharein — ek galat date ya wrong diagnosis code se rejection ho sakta hai

Important Helplines Aur Portals

| Resource | Contact | Purpose |

|---|---|---|

| IRDAI Bima Bharosa | bimabharosa.irdai.gov.in | Insurance complaint portal |

| IRDAI Helpline | 155255 / 1800 4254 732 | Toll-free complaint |

| IRDAI Email | complaints@irdai.gov.in | Email complaint |

| Insurance Ombudsman | cioins.co.in | Free dispute resolution (Rs 50L tak) |

| Consumer Court (Online) | e-daakhil.nic.in | Consumer complaint filing |

| National Consumer Helpline | 1800-11-4000 | Consumer rights helpline |

FAQ — Insurance Claim Reject Ke Common Questions

Q: Insurance claim reject hone ke baad kitne din mein action lena chahiye? A: Turant. GRO ko complaint 15 din mein result deni chahiye. Ombudsman mein rejection ke 1 saal ke andar jaana zaroori hai. Consumer Court mein 2 saal ka limitation hai. Jaldi action lena better hai.

Q: Insurance Ombudsman mein complaint karne mein kitna kharcha lagta hai? A: Zero. Bilkul free. Koi fee nahi, lawyer bhi mandatory nahi. Rs 50 lakh tak ke claims handle hote hain. Yeh sabse cost-effective remedy hai.

Q: Kya insurance company Ombudsman ke order ko ignore kar sakti hai? A: Nahi. Ombudsman ka award insurer pe binding hai — ignore karna legal violation hai. Agar company comply nahi karti toh IRDAI action le sakti hai plus aap consumer court ja sakte hain.

Q: Moratorium Rule (8 saal rule) kya hai exactly? A: IRDAI ke 2024 guidelines ke under — agar aapne 8 saal continuously premium bhara hai toh company pre-existing disease ke basis pe claim reject nahi kar sakti. Sirf proven fraud mein deny kar sakti hai. Yeh rule bahut strong protection hai.

Q: Kya consumer court mein insurance company ke against jeeta ja sakta hai? A: Haan, bahut frequently. Consumer courts regularly insurance companies ke against orders dete hain — claim amount + interest (9-12%) + compensation (mental harassment ke liye) + litigation cost. Courts isko “deficiency of service” maanti hain.

Q: Health insurance mein TPA ne claim reject kiya — company responsible hai ya TPA? A: Company responsible hai. TPA (Third Party Administrator) sirf company ki agent hai — final decision company ka hai. Complaint company ke against karo, TPA ke against nahi.

Q: Kya insurance claim reject letter milne ke baad bhi claim re-submit kar sakte hain? A: Haan. Agar aapke paas additional documents ya evidence hai jo rejection counter karta hai, toh company ko phir se review ke liye bhej sakte hain. But formally GRO complaint karna better approach hai — timeline aur accountability clear rehti hai.

Reject Accept Mat Karo — Fight Karo, Paisa Leke Aao

Insurance claim reject hona frustrating hai — but yeh end nahi hai. India mein aapke paas strong legal options hain. GRO, IRDAI Bima Bharosa, Insurance Ombudsman (free + binding), aur Consumer Court — 4 tier ka system aapke favour mein kaam karta hai.

Yaad rakhein:

- Insurance claim reject ka letter milte hi turant action lo — delay mat karo

- Pehle GRO ko written complaint karo — 15 din ka deadline hai unka

- GRO se satisfaction na mile toh IRDAI Bima Bharosa portal pe jaao

- Ombudsman free hai, Rs 50 lakh tak ke claims handle karta hai, aur order binding hai insurer pe

- Consumer Court mein claim + interest + compensation sab milta hai

- 8 saal ka Moratorium Rule — company pre-existing disease excuse nahi de sakti

- Rejection letter written mein maango — yeh sabse important document hai

- Har premium receipt, har medical record, har email save rakhein — yeh aapke proof hain

DuoCounsel ke podcast pe humne insurance disputes pe detailed episode kiya hai — real case studies ke saath. Zaroor sunein. Aur agar aapke saath insurance claim reject hua hai toh comment mein poochein — hum practicing advocates hain aur guide karenge.

About the Author

Adv. Barkha Jain & Adv. Yogesh Solanki (Founders, Duo Counsel)

Hum Duo Counsel hain—Adv. Barkha Jain aur Adv. Yogesh Solanki. Hum Gurugram District Courts aur Punjab & Haryana High Court mein as legal advocates practice karte hain.

Hamari legal expertise Matrimonial Disputes (Divorce/498A), Corporate Litigation, Cyber Crime aur New Criminal Laws (BNS/BNSS/BSA) mein aati hai. Aaj kal har doosre case mein clients hamare paas apne phone bhar ke messages lekar aate hain aur poochte hain ki inhe kanooni roop se court mein kaise istemal kiya jaye.

Digital duniya ke kanoon bohot complex hote hain. Hamara primary mission hai is kanooni jargon ko aasan Hinglish mein todkar aam citizens aur business owners ko unke aadhikar samjhana. Court mein digital evidence admit karwane ka humara ek lamba practical anubhav hai. Agar aap apne kisi important case mein WhatsApp Chat as Evidence ko technically aur legally theek dhang se pesh karwana chahte hain, toh hamari experts ki team aapki poori madad karne ke liye tayyar hai.

Kanoon Samjhein, Apne Saboot Sambhalein, Aur Secure Rahein!

- Platform: DuoCounsel.com

- Podcast: Duo Counsel Podcast (Available on YouTube & Spotify)

- Instagram: instagram.com/duocounsel

(Disclaimer: Yeh article sirf educational purposes aur legal awareness ke liye likha gaya hai. Kanoon (jaise BSA) ki interpretations courts dwara continuously update hoti rehti hain. Kripya is article ko apni personal professional legal advice ka direct substitute na maane. Koi bhi electronic evidence court mein pesh karne ya legal action lene se pehle apne personal advocate se zaroor consult karein.)