Hospital mein emergency admission hui. Bill dekhe — Rs 2.5 lakh. Aapke paas health insurance policy hai — Rs 10 lakh cover ki. Sab sahi hai na? Lekin tab pata chalta hai ki health insurance claim karne ka process kya hai, kab inform karna hai, kaunse documents chahiye — isme confusion hota hai. Aur ek galti karne se poora health insurance claim reject bhi ho sakta hai.

Main ek practicing advocate hoon aur maine personally health insurance claim ke bahut cases handle kiye hain — cashless reject huey, reimbursement delay hua, partial payment mila — sab situations. Aur sabse important baat — agar aap health insurance claim ka sahi process follow karte hain, toh 95%+ cases mein claim mil jaata hai.

Is article mein main aapko detail mein bataunga — health insurance claim kaise kare 2026 mein, cashless aur reimbursement claim ka difference, complete step-by-step process, kaunse documents chahiye, IRDAI ke naye 2026 rules, claim reject hone ke common reasons, aur agar aapka health insurance claim reject ya delay ho toh kya karein.

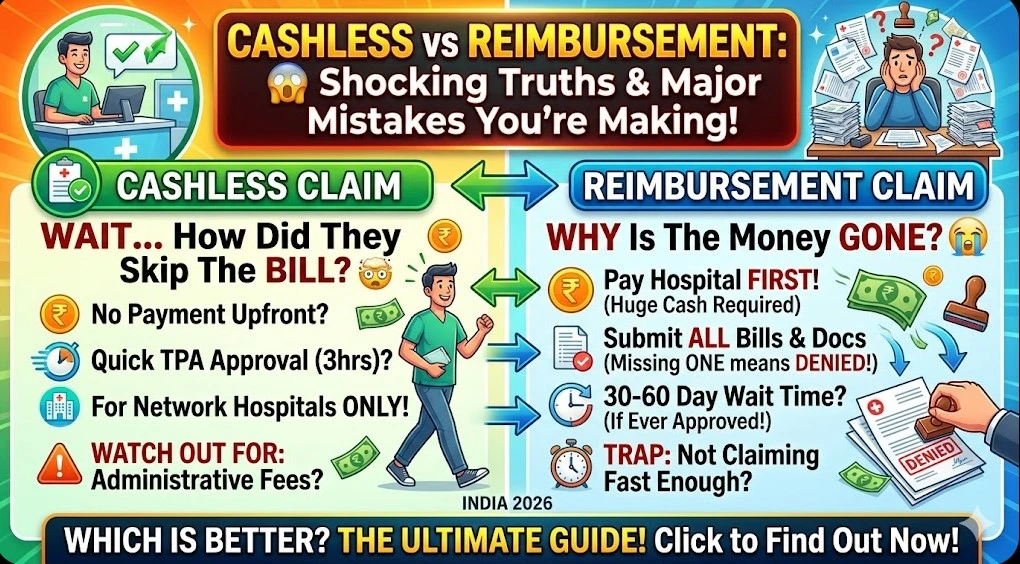

Quick Answer: Health insurance claim ke 2 tarike hain — Cashless (network hospital mein, insurer seedha hospital ko pay karta hai) aur Reimbursement (aap pehle pay karte hain, baad mein insurer se refund lete hain). Planned admission mein 48-72 ghante pehle insurer ko inform karo. Emergency mein 24 ghante ke andar. IRDAI ke 2024 Master Circular ke under cashless approval 1 ghante mein aur final discharge 3 ghante mein mandatory hai. Cashless reject ho toh reimbursement claim file karo — insurer ko 30 din mein settle karna hota hai.

Health Insurance Claim Kya Hai — Basic Samajh

Health insurance claim ek formal request hai insurance company ko — medical treatment ke kharche ko cover karne ke liye. Jab aapko hospital mein admit karna padta hai, ya planned surgery karwani hoti hai, tab health insurance claim submit kiya jaata hai.

India mein health insurance claim ke 2 main types hain:

1. Cashless Health Insurance Claim

- Network hospital mein treatment hota hai

- Insurer seedha hospital ko pay karta hai

- Aapko apni jeb se paisa nahi dena padta (sirf non-covered expenses ke liye)

- Sabse convenient aur stress-free option

2. Reimbursement Health Insurance Claim

- Aap pehle hospital ko poora pay karte hain

- Phir documents submit karke insurer se refund lete hain

- Non-network hospital mein use hota hai

- Ya jab cashless request reject ho jaaye

IRDAI ke data ke mutaabik — FY24 mein 3.1 crore se zyada health insurance claim file hue, jismein se approximately 8-12% reject ya partially settle hue. Matlab har 10 mein se 1 claim mein problem aati hai — mostly due to incorrect process.

Advocate’s Note: Health insurance claim file karne se pehle policy document padho — especially exclusions, sub-limits, waiting periods aur room rent cap. Yeh basic knowledge aapka health insurance claim smoothly process karne mein help karegi. 80% rejection ki wajah policy terms ki unawareness hai.

Cashless Health Insurance Claim — Complete Step-by-Step Process

Cashless process sabse preferred hai kyunki stress-free hai. Yeh detail mein samjho.

Step 1: Network Hospital Check Karo

Har insurer ki network hospital list hoti hai. Cashless health insurance claim sirf network hospital mein hi possible hai. Check karne ke tarike:

- Insurer ki website pe “Network Hospital” section

- TPA app (Health TPA, Paramount, Raksha, etc.)

- Toll-free number pe call karo

- Insurer ka mobile app (Star Health, HDFC ERGO, Niva Bupa apps)

2026 Update: IRDAI ke “Cashless Everywhere” initiative ke under, kuch cases mein non-network hospital mein bhi cashless possible hai — 48 ghante pehle insurer ko inform karke.

Step 2: Pre-Authorization Request Karo

Planned admission (scheduled surgery, hospitalization):

- 48-72 ghante pehle insurer/TPA ko inform karo

- Hospital ka insurance desk help karega

Emergency admission:

- 24 ghante ke andar insurer ko inform karna zaroori hai

- Agar late hua toh health insurance claim reimbursement mein convert ho sakta hai

Pre-authorization form mein yeh details bharni hoti hain:

- Patient details (name, policy number, age)

- Hospital details aur admission date

- Diagnosis aur proposed treatment

- Estimated treatment cost

- Treating doctor ka naam aur qualification

- Prior medical history

Step 3: TPA/Insurer Review Karega

TPA (Third Party Administrator) — yeh insurer ki behalf pe claim process karta hai. IRDAI 2024 Master Circular ke under:

- 1 ghante ke andar pre-authorization decision aana chahiye

- Approval, partial approval, ya rejection — teen mein se ek

Pre-Authorization Approval Letter (PAL) mein yeh hota hai:

- Approved amount (jo initial estimate hai)

- Policy number aur claim ID

- Treatment cover confirmation

- Room category approved

Important: PAL final bill nahi hai — final amount discharge pe tay hota hai actual bills ke basis pe.

Step 4: Treatment Lein Aur Hospital Stay

- Hospital aapka treatment karega normal tarike se

- Non-medical expenses (food, attendant, phone charges) aapko khud pay karne hote hain

- Discharge ke waqt final bill prepare hoga

Step 5: Discharge Authorization

Discharge ke waqt hospital insurer ko final bill bhejega. IRDAI rules ke under:

- 3 ghante ke andar final authorization aana chahiye

- Agar insurer delay karta hai aur additional charges lagte hain (extra room rent), woh insurer ko bear karna hota hai

- Aap ek receipt sign karte ho non-covered amount ke liye

Step 6: Discharge Aur Payment Settlement

- Insurer seedha hospital ko approved amount pay karta hai

- Aap non-covered expenses (co-pay, sub-limit excess, non-medical items) pay karte ho

- Complete bill copy apne paas rakhein

Reimbursement Health Insurance Claim — Complete Process

Reimbursement health insurance claim tab file hota hai jab:

- Aap non-network hospital mein admit hue ho

- Cashless request reject ho gayi

- Emergency mein insurer ko time pe inform nahi kar paye

- Pre ya post-hospitalization expenses claim karne hain

Step 1: Treatment Ke Dauraan Sab Documents Collect Karo

Day 1 se collect karna shuru karo:

- Saari investigation reports (X-ray, MRI, blood tests)

- Doctor ki prescriptions aur consultation papers

- Admission notes

- Daily medical records

- Medicine bills (pharmacy se)

- Implants/prosthetics ke bills (agar applicable)

Step 2: Hospital Bill Pay Karo

- Discharge ke waqt complete bill pay karo

- Original receipts maango — photocopy accept nahi hoti

- Itemized bill maango — room rent, medicines, procedures, doctor fees alag-alag

- Payment proof (cash receipt, card swipe slip)

Step 3: Discharge Summary Aur Final Papers Lein

Hospital se leaving se pehle yeh lein:

- Discharge Summary (original, signed by doctor)

- Operation notes (surgery hui toh)

- Final itemized bill

- Pharmacy bills

- Payment receipts

- Implant stickers aur invoice (agar implant use hua)

Step 4: Health Insurance Claim Form Bharo

IRDAI-standard claim form mein 2 parts hote hain:

- Part A: Policyholder/Patient fills — personal details, hospitalization details, bank details

- Part B: Treating doctor fills — diagnosis, treatment, prognosis

Dono parts carefully bharein — koi bhi field khaali nahi chhodein.

Step 5: Complete Document Set Submit Karo

Reimbursement health insurance claim ke liye yeh documents chahiye:

| Document | Original/Copy |

|---|---|

| Claim form (Part A + B) | Signed original |

| Discharge summary | Original |

| Final itemized hospital bill | Original |

| Payment receipts | Original |

| All investigation reports | Originals |

| Pharmacy bills with prescriptions | Originals |

| Pre-authorization letter (agar mila tha) | Copy |

| Policy copy | Copy |

| KYC — Aadhaar + PAN | Copy |

| Cancelled cheque / bank details | Copy |

| FIR copy (accident case mein) | Copy |

| Pre-post hospitalization bills | Originals |

Step 6: Submission Aur Follow-Up

- 15-30 din ke andar discharge ke baad submit karo

- Submission 2 tareeke se hoti hai:

- Online: Insurer portal ya app pe upload karo

- Offline: Branch office mein physical submission (acknowledgement slip lein)

- Claim acknowledgement zaroor lo — “last document received” date important hai

Step 7: Settlement Timeline

IRDAI rules ke under:

- 30 din ke andar health insurance claim settle hona mandatory hai (last document submission date se)

- Delay pe insurer ko 2% above bank rate interest dena hota hai

- 45 din se zyada delay = clear violation hai IRDAI rules ka

Health Insurance Claim Ke Liye Required Documents — Complete Checklist

Yeh sabse important section hai. Documents missing hone se 40%+ health insurance claim reject hote hain.

Cashless Claim Ke Liye:

- Health card / Policy copy (mandatory)

- Government ID — Aadhaar, PAN, Passport

- Doctor’s admission advice

- Pre-authorization form (hospital insurance desk fill karega)

- Previous medical records (pre-existing condition disclose karne ke liye)

- Attendant KYC (kuch insurers maangte hain)

Reimbursement Claim Ke Liye (Zyada Extensive):

- Sab cashless documents

- Claim form (Part A + B, signed)

- Original discharge summary

- Original itemized hospital bill

- All original payment receipts

- All investigation reports (X-ray, MRI, blood work, biopsy)

- Pharmacy bills with matching prescriptions

- Operation notes (surgery case mein)

- Anaesthesia notes (agar anaesthesia hui)

- Implant stickers + invoice (implant use hua toh)

- Cancelled cheque / bank account details

- Cashless denial letter (agar cashless reject hua tha)

- FIR copy (road accident, burns, poisoning cases mein)

- Pre-hospitalization bills (30-60 din pehle ke, policy ke hisab se)

- Post-hospitalization bills (60-180 din baad ke)

Pro Tip: Har health insurance claim submit karne se pehle scanned copies banake rakho — agar insurer original documents kho de, aapke paas proof hoga. Digital organize karo — folder mein date aur procedure ke hisab se.

IRDAI 2026 Naye Rules — Har Policyholder Ko Jaanni Chahiye

2024 ke Master Circular aur 2026 ke updates ne health insurance claim process ko transform kar diya hai.

1. Cashless Everywhere Initiative

- Non-network hospitals mein bhi cashless health insurance claim possible hai

- 48 ghante pehle (planned) ya 15 ghante mein (emergency) inform karna hota hai

- Insurer refuse nahi kar sakta agar genuine hospital hai

2. Moratorium Period Reduction — 8 Se 5 Saal

- Pehle 8 saal tha, ab 5 saal continuous premium bharne ke baad

- Company pre-existing disease ke basis pe claim reject nahi kar sakti

- Sirf proven fraud case mein deny kar sakti hai

3. Pre-Existing Disease Waiting Period — 24 Months Max

- Pehle 48 months tak tha

- Ab maximum 24 months (2 saal) hai

- 2 saal baad pre-existing disease related health insurance claim valid hai

4. Time-Bound Settlement — Strict Timelines

- Cashless approval: 1 ghante mein

- Discharge authorization: 3 ghante mein

- Reimbursement settlement: 30 din mein

- Delay = interest + IRDAI action

5. No Upper Age Limit

- Ab koi maximum age limit nahi hai policy kharidne ke liye

- Senior citizens ko comprehensive health insurance claim protection

6. GST Exemption (September 2025 Se)

- Individual health policy premium pe 18% GST hata diya gaya

- Premium ab 18% sasta ho gaya effectively

7. Lifetime Renewal Guaranteed

- Insurer policy renewal refuse nahi kar sakta

- Chahe claim kiya ho ya age badh gayi ho

- Sirf proven fraud case mein denial allowed

Health Insurance Claim Reject Kyun Hota Hai — 10 Common Reasons

Health insurance claim reject hone se bachne ke liye yeh reasons jaan lo:

1. Pre-existing Disease Non-Disclosure

Policy lete waqt diabetes, BP, heart condition nahi bataayi — baad mein usi se related treatment hua. Top rejection reason.

2. Waiting Period Incomplete

Maternity (2 saal), specific diseases (1-4 saal), pre-existing (2-4 saal) ke waiting periods. Is time mein claim nahi milta.

3. Excluded Treatments

Cosmetic surgery, infertility treatment, dental (unless accident), mental health (kuch policies mein) exclude hote hain.

4. Hospitalization Nahi Zaroori Thi

TPA kehta hai “yeh OPD case tha, admission nahi chahiye tha.” Doctor ki notes strong honi chahiye.

5. Sub-Limit Exceeded

Room rent cap, ICU sub-limit, disease-specific caps exceed ho gaye. Proportionate deduction hota hai.

6. Delayed Claim Submission

15-30 din ki deadline miss ki. Late submission pe health insurance claim reject hota hai ya interest nahi milta.

7. Incomplete/Wrong Documents

Discharge summary missing, unsigned forms, photocopies submitted — 40% rejections ka reason.

8. Policy Lapsed Premium Nahi Bhara

Grace period bhi miss ho gayi — policy lapsed. Treatment date pe policy active nahi thi.

9. Treatment Exclusion List Mein Hai

Experimental treatment, non-allopathic therapies (kuch policies mein), cosmetic procedures.

10. Room Rent Proportionate Deduction

Policy mein Rs 5,000/day cap tha, aapne Rs 15,000 ka room liya. Sab associated charges (doctor visits, nursing) bhi proportionately cut hote hain.

Health Insurance Claim Reject Ho Toh Kya Kare — 4-Tier Recovery

Tier 1: Insurer Ka Grievance Redressal Officer (GRO)

Written complaint bhejo — email + registered post. 15 din mein response mandatory.

Tier 2: IRDAI Bima Bharosa Portal

bimabharosa.irdai.gov.in pe complaint register karo. Helpline: 155255 / 1800 4254 732.

Tier 3: Insurance Ombudsman (FREE, Binding Order)

cioins.co.in — Rs 50 lakh tak ke health insurance claim disputes. 1 saal ke andar file karo.

Tier 4: Consumer Court

Also read:- UPI Fraud Hua Toh Paisa Kaise Wapas Le 2026 — 7-Step Recovery Process Jo Har Victim Ko Jaanni Chahiye

e-daakhil.nic.in — claim + 9-12% interest + mental harassment compensation + litigation cost milta hai.

Also Read :- Insurance Claim Reject Hua Toh Kya Kare 2026 — IRDAI, Ombudsman Aur Consumer Court Ka Pura Process

Real Case Study — Rs 3.6 Lakh Ka Health Insurance Claim Recovery

Background: Mr. Arun (45), Gurugram. Policy: Rs 10 lakh family floater, 4 saal purani. Papa ko heart attack aaya — angioplasty surgery karwani padi. Bill: Rs 3,60,000.

Problem: Cashless health insurance claim submit kiya — TPA ne reject kiya, reason: “Pre-existing hypertension was not disclosed at policy inception.”

Action Taken:

- Family ne Rs 3.6 lakh khud pay kiya discharge pe

- Reimbursement health insurance claim file ki complete documents ke saath

- Medical records attach kiye — prove kiya ki hypertension diagnosis policy ke 2 saal baad hua

- Insurer ne 45 din baad Rs 1.8 lakh partial payment offer kiya

- GRO ko written appeal — detail mein clarification

- 20 din mein partial response — Rs 2.4 lakh offer

- Insurance Ombudsman ke paas gaye — complete documents ke saath

- Hearing hui — medical records ne prove kiya hypertension post-policy developed

Ombudsman Order:

- Company ka rejection unjustified

- Rs 3,60,000 full claim pay karein

- Rs 40,000 compensation for mental harassment aur delay

- Rs 25,000 interest @ 2% above bank rate (120 din delay ke liye)

- Total recovery: Rs 4,25,000

Timeline: Rejection se Ombudsman decision tak — 5.5 months.

Lesson: Health insurance claim reject hone pe give up mat karo. System aapke favour mein hai.

Health Insurance Claim Mein Bachne Ke 10 Smart Tips

- Policy document padho policy milne ke 15-30 din mein (free look period mein cancel kar sakte ho)

- Sab pre-existing conditions disclose karo — chhupana sabse bada risk hai

- Network hospitals ki list save karo phone mein — emergency mein kaam aayegi

- TPA ka helpline number mobile mein feed karo

- Annual health check-up karwao — preventive care covered hota hai + policy history clean rehti hai

- Premium time pe bharein — grace period bhi miss karne se policy lapse hoti hai

- Har bill aur report store karo — digital + physical dono mein

- Health insurance claim file karne mein jaldi karo — deadline pe mat karo

- Doctor se proper documentation maango — medical necessity clearly likhwao

- Room category policy ke hisab se choose karo — sub-limit se zyada room = proportionate cuts

FAQ — Health Insurance Claim Ke Common Questions

Q: Health insurance claim file karne ki deadline kya hai? A: Cashless mein planned admission se 48-72 ghante pehle, emergency mein 24 ghante ke andar. Reimbursement mein discharge ke 15-30 din ke andar (policy ke hisab se). Deadline miss karne pe claim reject ho sakta hai.

Q: Cashless reject ho jaaye toh kya karein? A: Treatment normally complete karo — paisa khud pay karo. Phir reimbursement health insurance claim file karo complete documents ke saath. IRDAI rule ke under insurer ko 30 din mein settle karna hota hai.

Q: Pre-existing disease ke liye health insurance claim kab milta hai? A: 2026 rules ke under maximum 2 saal ka waiting period hai pre-existing diseases pe. 5 saal continuous premium bharne ke baad Moratorium Rule lagta hai — company claim reject nahi kar sakti PED ground pe.

Q: Ek policy mein saal mein kitni baar health insurance claim kar sakte hain? A: Jitni baar zaroorat ho — sum insured exhaust hone tak. Example: Rs 10 lakh cover hai, aap 3 baar Rs 3 lakh ka claim kar sakte ho saal mein. Limit sum insured hai, not number of claims.

Q: Cashless mein poora bill cover hota hai ya kuch khud dena padta hai? A: Policy covered expenses insurer pay karta hai. Non-medical items (food, phone, attendant), room rent excess, co-pay, sub-limit excess, consumables (syringes, gloves — kuch policies mein) aapko pay karne hote hain.

Q: Agar insurer 30 din mein reimbursement nahi karta toh? A: IRDAI rule ke under insurer ko 2% above bank rate interest dena hota hai delay pe. GRO ko complaint karo pehle, phir Bima Bharosa portal pe, phir Insurance Ombudsman — yeh escalation path hai.

Q: Health insurance claim ke liye lawyer zaroori hai? A: Simple cases mein nahi — aap khud file kar sakte ho. Lekin agar claim reject ho aur amount Rs 1 lakh+ hai, ya complex medical interpretation hai, toh advocate consult karna smart hai. Insurance Ombudsman mein lawyer mandatory nahi hai.

Insurance Aapka Haq Hai — Claim Karo, Paisa Paao

Health insurance claim process complex lagta hai — but actually systematic hai. Agar aap steps sahi follow karte ho, documents complete rakhte ho, aur IRDAI rules jaante ho, toh 95%+ cases mein health insurance claim smoothly mil jaata hai.

Yaad rakhein:

- Cashless health insurance claim preferred hai — network hospital check karo pehle

- Planned admission: 48-72 ghante pehle inform karo

- Emergency admission: 24 ghante ke andar inform karna mandatory hai

- IRDAI 2026 rules — 1 ghanta cashless approval, 3 ghante discharge, 30 din reimbursement

- Moratorium rule ab 5 saal ka hai — pre-existing disease excuse nahi chalega

- Health insurance claim reject ho toh 4-tier system use karo — GRO, IRDAI, Ombudsman, Consumer Court

- Documents complete rakho — 40% rejections incomplete docs se hote hain

- Insurance Ombudsman free hai aur order binding hota hai insurer pe

- Har medical bill aur record digital + physical dono store karo

DuoCounsel ke podcast pe humne health insurance disputes pe detailed episode kiya hai — real case studies ke saath. Zaroor sunein. Aur agar aapka health insurance claim reject ya delay ho raha hai, toh comment mein poochein — hum practicing advocates hain aur guide karenge.

About the Author

Adv. Barkha Jain & Adv. Yogesh Solanki (Founders, Duo Counsel)

Hum Duo Counsel hain—Adv. Barkha Jain aur Adv. Yogesh Solanki. Hum Gurugram District Courts aur Punjab & Haryana High Court mein as legal advocates practice karte hain.

Hamari legal expertise Matrimonial Disputes (Divorce/498A), Corporate Litigation, Cyber Crime aur New Criminal Laws (BNS/BNSS/BSA) mein aati hai. Aaj kal har doosre case mein clients hamare paas apne phone bhar ke messages lekar aate hain aur poochte hain ki inhe kanooni roop se court mein kaise istemal kiya jaye.

Digital duniya ke kanoon bohot complex hote hain. Hamara primary mission hai is kanooni jargon ko aasan Hinglish mein todkar aam citizens aur business owners ko unke aadhikar samjhana. Court mein digital evidence admit karwane ka humara ek lamba practical anubhav hai. Agar aap apne kisi important case mein WhatsApp Chat as Evidence ko technically aur legally theek dhang se pesh karwana chahte hain, toh hamari experts ki team aapki poori madad karne ke liye tayyar hai.

Kanoon Samjhein, Apne Saboot Sambhalein, Aur Secure Rahein!

- Platform: DuoCounsel.com

- Podcast: Duo Counsel Podcast (Available on YouTube & Spotify)

- Instagram: instagram.com/duocounsel

(Disclaimer: Yeh article sirf educational purposes aur legal awareness ke liye likha gaya hai. Kanoon (jaise BSA) ki interpretations courts dwara continuously update hoti rehti hain. Kripya is article ko apni personal professional legal advice ka direct substitute na maane. Koi bhi electronic evidence court mein pesh karne ya legal action lene se pehle apne personal advocate se zaroor consult karein.)