Aapki dadi ka sona, family ke important documents, FD certificates, property papers — sab bank locker mein “safe” rakhe hain. Aap nishchint hain — “Bank mein hai, kuch nahi hoga.” Phir ek din khabar aati hai — bank branch mein chori hui, lockers tode gaye. Ya building mein aag lagi. Ya bank employee ne hi locker se cheezein nikaal li.

Ab sawaal — kya bank aapka nuksan bharega? Kitna? Kaise?

Yeh wo sawaal hai jiska answer 90% locker holders ko nahi pata. Bank locker ke rules ke baare mein sabse bada myth yeh hai ki “bank poori responsibility leta hai.” Sach iske bilkul ulta hai — bank ki liability bahut limited hai, aur kuch cases mein bilkul zero.

Main ek practicing advocate hoon aur Gurugram mein consumer aur banking disputes regularly handle karta hoon. Bank locker ke rules — yeh har us insaan ko jaanne chahiye jiska bank locker hai. 2021 mein Supreme Court (Amitabha Dasgupta v. United Bank of India) aur RBI ne yeh rules completely clear kiye — kab bank liable hai, kab nahi, aur kitna compensation milta hai.

Is complete evergreen guide mein main bataunga — bank locker ke rules kya hain, locker ki legal nature, Supreme Court judgment, RBI guidelines, bank kab liable hai aur kab nahi, 100x rent cap, compensation kaise claim karein, aur apni valuables kaise protect karein.

Quick Answer: Bank locker ke rules ke according — bank ki liability limited hai. RBI 2021 guidelines (effective Jan 2022) ke under, agar nuksan bank ki negligence se hua (theft, robbery, fire, building collapse, ya employee fraud) — toh bank annual locker rent ka maximum 100 times compensate karega. Lekin agar nuksan natural calamity / Act of God (earthquake, flood, lightning) ya customer ki apni galti se hua — bank bilkul liable nahi. Amitabha Dasgupta v. United Bank of India (2021) SC ne establish kiya — bank “no liability” claim nahi kar sakta, due diligence owe karta hai. Compensation ke liye: Bank complaint → Banking Ombudsman → Consumer Court. Locker contents ka koi insurance bank nahi deta — apni valuables ka separate insurance lena better hai.

Also Read :- Child Custody Laws India — Guardian Wards Act Ke Under Complete Rights Aur Process

Bank Locker Ki Legal Nature — Bailment Ya Tenancy?

Bank locker ke rules samajhne ke liye pehle yeh jaano ki legally locker relationship kya hai.

Purana View — Banks Ka “No Liability” Stand

Decades tak banks yeh stand lete the:

- “Hum locker contents ke baare mein nahi jaante”

- “Hum sirf space rent pe dete hain — landlord-tenant relationship hai”

- “Contents ki responsibility customer ki hai”

- “Hum liable nahi hain kisi loss ke liye”

Locker agreements mein one-sided clauses hote the jo bank ko completely absolve karte the.

Supreme Court Ka New View (Amitabha Dasgupta 2021)

Supreme Court ne is “no liability” stand ko reject kiya:

“Banks cannot wash off their hands and claim that they bear no liability towards their customers for the operation of the locker.”

Court ne kaha — bank aur customer ke beech bailor-bailee jaisa duty of care hota hai. Bank ko due diligence maintain karni padti hai. “Contents nahi jaante” yeh excuse liability se bachne ke liye valid nahi hai.

Advocate’s Note: Bank locker ke rules mein sabse important shift yeh hai — pehle banks “tenancy” argument se completely escape karte the. Ab Supreme Court ne clearly kaha ki banks ko minimum standard of care maintain karni hi padegi — woh contract se bhi waive nahi kar sakte. Lekin — aur yeh critical hai — yeh liability unlimited nahi hai. RBI ne 100x rent cap laga diya. Toh customers ko realistic expectations rakhni chahiye aur high-value items ke liye separate insurance sochna chahiye.

Amitabha Dasgupta v. United Bank Of India (2021) — Landmark Judgment

Yeh bank locker ke rules ka foundational case hai.

Case Facts:

- Mr. Amitabha Dasgupta (Kolkata resident) ki maa ne 1950s mein United Bank of India mein locker liya tha

- Dispute hua locker rent ko lekar

- Bank ne locker break open kar diya — galat tarike se, despite dues cleared the

- Contents missing ho gaye

- Dasgupta ne consumer forum mein case kiya — National Consumer Commission tak gaya

Supreme Court Ka Decision (19 February 2021):

Justices M.M. Shantanagoudar aur Vineet Saran ki bench ne:

- Bank ko gross negligence ka doshi thehraya — improper locker break-open

- Rs 5 lakh compensation + Rs 1 lakh litigation cost imposed

- Compensation erring officers ki salary se deduct hone ka order

- RBI ko direct kiya — 6 mahine mein comprehensive locker rules banao

- Jab tak RBI rules na aaye — court ke principles binding rahenge

Key Principles Established:

- Banks “no liability” claim nahi kar sakte

- Banks ko due diligence maintain karni hogi locker safety mein

- Banks unilateral unfair terms impose nahi kar sakte

- Locker break-open mein proper procedure mandatory (notice, witnesses, inventory)

- Banks ke saath customer “completely at mercy” hai — isliye bank ki responsibility zyada

RBI Locker Rules 2021 — Complete Framework

Supreme Court ke directive ke baad, RBI ne August 2021 mein revised locker guidelines jaari kiye — 1 January 2022 se effective (full implementation Jan 2023).

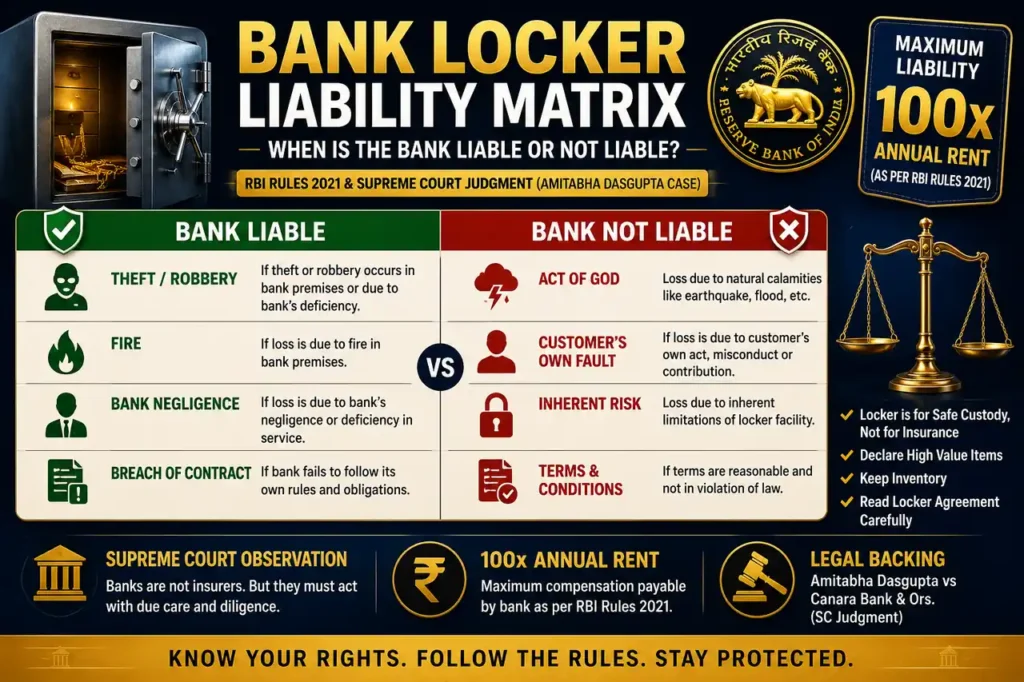

Bank Ki Liability — Kab Aur Kitni

RBI 2021 ke under bank LIABLE hai (100x annual rent tak):

| Situation | Bank Liable? |

|---|---|

| Theft / Robbery at branch | ✅ Yes — 100x rent |

| Fire | ✅ Yes — 100x rent |

| Building collapse | ✅ Yes — 100x rent |

| Employee fraud (bank staff ne churaya) | ✅ Yes — 100x rent |

| Bank’s negligence in security | ✅ Yes — 100x rent |

Bank NOT LIABLE:

| Situation | Bank Liable? |

|---|---|

| Natural calamity (earthquake, flood, lightning) — Act of God | ❌ No |

| Customer’s own negligence | ❌ No |

| War, riots (force majeure) | ❌ Generally no |

Condition for Act of God exemption: Bank ko phir bhi reasonable care leni padti hai premises protect karne ke liye. Agar bank ne basic precautions nahi liye — exemption nahi milega.

100x Rent Cap — Practical Example

RBI rule: Bank ki liability = Maximum 100 times annual locker rent

Example calculation:

- Aapka annual locker rent: Rs 3,000

- Bank ki maximum liability: Rs 3,000 × 100 = Rs 3,00,000

Problem: Agar locker mein Rs 20 lakh ka sona tha aur chori ho gaya — bank sirf Rs 3 lakh dega (agar negligence proved). Baaki Rs 17 lakh ka koi compensation nahi.

Yeh sabse critical point hai bank locker ke rules mein — liability rent-based hai, contents-value based nahi.

Locker Agreement Ke Key Terms — Kya Dekhein

Bank locker ke rules ke under, RBI ne locker agreement standardize kiya hai. Agreement sign karte waqt yeh check karo:

Mandatory Provisions (RBI 2021):

- Copy of agreement — bank ko allotment ke time aapko dena mandatory

- Clear liability terms — bank ki responsibility clearly mentioned

- Prohibited items clause — illegal/hazardous items nahi rakh sakte

- Rent terms — annual rent, payment schedule

- Break-open conditions — kab bank break kar sakta hai

- Nomination facility — death ke baad kaun access karega

Prohibited Items (Locker Mein Nahi Rakh Sakte):

- Cash / currency (kuch banks allow karte hain, kuch nahi — agreement check karo) bank locker ke rules

- Illegal substances — drugs, contraband

- Weapons, explosives

- Hazardous materials

- Perishable items

- Radioactive material

- Anything illegal under law

Agar prohibited items se nuksan hua — bank bilkul liable nahi.

Locker Break-Open Rules — Bank Kab Tod Sakta Hai

Bank locker ke rules mein break-open ke liye strict procedure hai (Amitabha Dasgupta case ke baad):

Bank Locker Break Kar Sakta Hai Jab:

- Rent default — 3 saal tak rent nahi diya (after notices)

- Locker abandoned — 7 saal tak operate nahi hua + rent paid (dormant) bank locker ke rules

- Court/authority order — legal direction

- Suspicious activity — security concern

Mandatory Break-Open Procedure:

- Written notice — locker holder ko reasonable time pehle

- Authorized officials ki presence

- Independent witness mandatory

- Inventory of contents — sab items ka detailed list

- Video recording (recommended best practice)

- Safe custody of contents until claimed

Agar bank ne proper procedure follow nahi ki — Amitabha Dasgupta case jaise gross negligence — compensation milta hai. bank locker ke rules

Nomination Facility — Death Ke Baad Kya Hota Hai

Bank locker ke rules mein nomination critical hai — yeh ensure karta hai ki death ke baad family ko access mile.

Nomination Types:

Single locker holder:

- Ek nominee register kar sakte ho

- Death ke baad nominee access kar sakta hai (inventory ke saath)

Joint locker holders:

- Survivor + nominee provisions

- “Either or survivor,” “former or survivor” — operation modes

Bina Nomination — Death Ho Jaaye Toh:

- Legal heirs ko succession certificate ya legal heir certificate chahiye

- Lengthy process — bank verification

- Court documents zaroori

DuoCounsel advice: Locker mein nomination zaroor register karo — bina nomination death ke baad family ko mahino tak access nahi milta. (Iske liye humne “Deceased Ki Property Par Claim” article mein detail diya hai.) bank locker ke rules

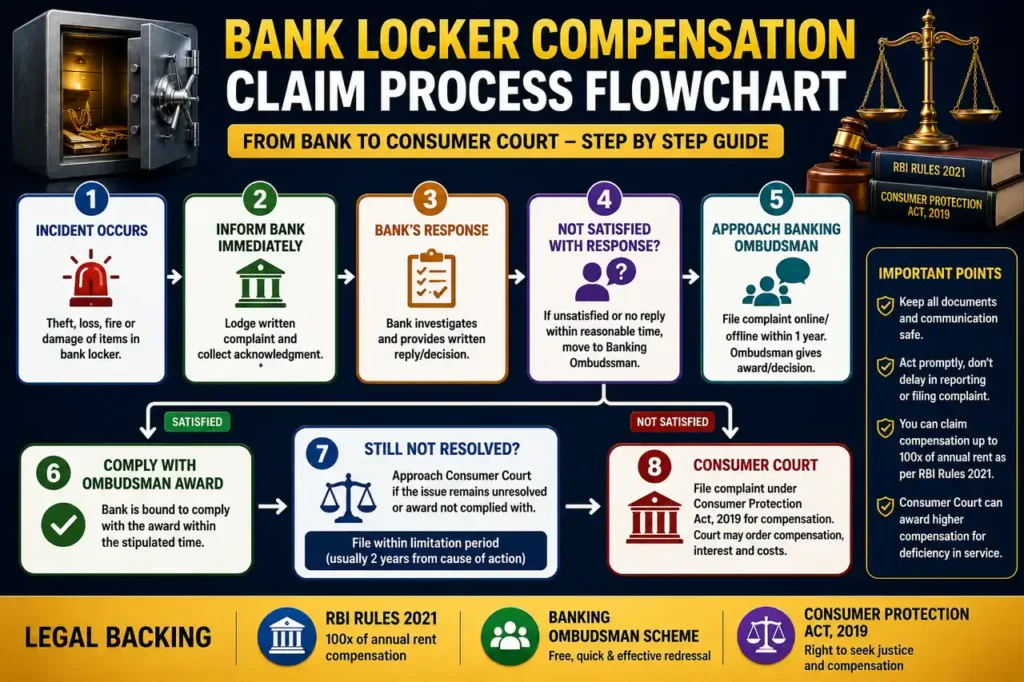

Compensation Kaise Claim Karein — Step By Step

Agar bank locker ke rules ke violation se aapko nuksan hua:

Step 1: Bank Ko Written Complaint

- Branch manager ko written complaint

- Incident details — kya hua, kab, kitna nuksan

- Locker agreement copy attach

- Bank ki negligence clearly establish karo

- Acknowledgment lo

Step 2: Bank Ki Internal Grievance

- Bank ka grievance redressal — Nodal Officer

- 30 din mein response expect karo

- Written record maintain karo

Step 3: Banking Ombudsman (RBI)

Agar bank satisfy na kare:

- RBI Banking Ombudsman — cms.rbi.org.in pe complaint

- Free — no fee

- Online complaint possible

- Ombudsman bank ko direct kar sakta hai compensation ka

Step 4: Consumer Court

Amitabha Dasgupta case ne confirm kiya — locker deficiency Consumer Protection Act ke under aati hai:

- District Consumer Commission (up to Rs 50 lakh)

- State Commission (Rs 50 lakh – 2 crore)

- Deficiency of service ground

- Compensation + mental harassment + costs

Step 5: Civil Suit (Large Claims)

Bahut large amounts ke liye civil court — lekin consumer court faster aur cheaper hai.

Apni Valuables Kaise Protect Karein — 8 Practical Tips

Bank locker ke rules ke limitations samajhne ke baad — yeh practical protection:

- Locker contents ki list maintain karo — kya kya rakha hai, photos ke saath (private record)

- High-value items ka separate insurance — bank locker insurance contents cover nahi karta — jewelry insurance lo

- Nomination zaroor register karo — death ke baad family access ke liye

- Rent time pe pay karo — default se locker break-open risk

- Locker regularly operate karo — dormant lockers (7 saal) break ho sakte hain

- Agreement copy sambhaalo — liability terms ka proof

- Receipts rakho — jewelry purchase bills (value proof for insurance + compensation)

- Branch security check karo — CCTV, guards, vault security — high-value items ke liye good branch choose karo

Insurance — Sabse Important Protection

Bank locker ke rules ki sabse badi limitation — 100x rent cap se zyada compensation nahi. Isliye:

- Jewellery insurance lo — Rs 20 lakh sona = separate insurance policy

- Home insurance riders — kuch policies locker contents cover karti hain

- Specific valuable insurance — high-value items ke liye

Insurance premium thoda kharcha hai, lekin Rs 20 lakh ki protection ke liye worth it hai — kyunki bank sirf Rs 3 lakh dega.

Bank Locker Vs Bank Liability — Reality Check Table

Bank locker ke rules ki reality clearly samajho:

| Customer Expectation | Legal Reality |

|---|---|

| “Locker 100% safe hai” | Bank ki limited liability hai |

| “Bank poora nuksan bharega” | Maximum 100x annual rent |

| “Sona safe hai bank mein” | Bank contents ka insurer nahi |

| “Bank responsible hai sab cheez ke liye” | Sirf bank negligence pe liable |

| “Natural disaster mein bank bharega” | Act of God = no liability |

| “Locker contents insured hain” | Koi automatic insurance nahi |

Real Case Study — Gurugram Locker Theft Compensation

Background: Mrs. Sunita (age 54), Gurugram. Ek private bank branch mein locker — 8 saal se. Annual rent Rs 4,000. Locker mein family gold (approximately Rs 12 lakh value) aur property documents.

Incident: Bank branch mein night burglary hui — gang ne vault tod ke 15 lockers break kiye. Sunita ka locker bhi — sara sona gaya, documents bach gaye.

Bank Ka Initial Response:

- “Hum contents ke baare mein nahi jaante”

- “Aapko prove karna hoga kya tha locker mein”

- “Liability limited hai”

Action Taken:

Week 1:

- DuoCounsel se consult kiya

- Bank ko written complaint — burglary, negligence (inadequate vault security)

- Police FIR copy (burglary ki)

- Jewellery purchase bills jo the (Rs 7 lakh ke documented)

Key Legal Points Established:

- Burglary = bank negligence (RBI rule — theft/robbery pe liable)

- Bank ki vault security inadequate thi — guard nahi tha night mein

- Amitabha Dasgupta principle — bank “no liability” claim nahi kar sakta

Week 4:

- Bank ne initially Rs 4 lakh offer kiya (100x rent = Rs 4,000 × 100 = Rs 4,00,000)

- Sunita ka actual loss Rs 12 lakh — gap Rs 8 lakh

Week 8:

- Banking Ombudsman complaint filed — bank ki security negligence highlight

- Parallel — District Consumer Commission complaint

Month 6:

- Consumer Commission ne bank ko negligent paya — inadequate security

- Bank ko 100x rent (Rs 4 lakh) + Rs 1 lakh mental harassment + Rs 25,000 costs pay karne ka order

- Total: Rs 5.25 lakh

Reality:

- Sunita ko Rs 5.25 lakh mila

- Rs 7 lakh ka loss recover NAHI hua — kyunki 100x cap limit thi

- Lesson: Agar jewellery insured hota — full Rs 12 lakh recover ho jata

Key Takeaways:

- Burglary mein bank liable hai — but only 100x rent

- 100x cap = major limitation — high value items ke liye insufficient

- Insurance hota toh — full recovery possible thi

- Documentation (bills) helped establish claim

- Consumer court + ombudsman — effective forums

FAQ — Bank Locker Ke Rules Ke Common Questions

Q: Bank locker mein chori ho jaaye toh bank kitna compensation deta hai? A: RBI 2021 rules ke under — agar chori bank ki negligence se hui (theft, robbery, employee fraud) — bank maximum 100 times annual locker rent deta hai. Example: Rs 3,000 annual rent = Rs 3 lakh maximum. Contents ki actual value se zyada nahi — yeh bank locker ke rules ki sabse important limitation hai.

Q: Kya bank locker contents insured hote hain? A: Nahi — bank locker contents ka koi automatic insurance nahi hota. Bank sirf negligence pe limited liability (100x rent) leta hai. High-value items (gold, jewellery) ke liye separate insurance policy leni chahiye. Yeh sabse important protection hai jo log ignore karte hain. bank locker ke rules

Q: Natural disaster (flood, earthquake) mein locker contents nuksan ho toh? A: RBI rules ke under — Act of God (earthquake, flood, lightning, thunderstorm) cases mein bank liable nahi hota. Lekin bank ko phir bhi reasonable care leni padti hai premises protect karne ke liye. Agar bank ne basic precautions nahi liye — partial liability ho sakti hai. Isliye insurance important hai.

Q: Bank ne meri locker bina notice tod di — kya kar sakta hoon? A: Yeh Amitabha Dasgupta case jaisa hi hai — gross negligence. Bank break-open ke liye proper procedure follow karni hoti hai — written notice, authorized officials, independent witness, inventory. Bina procedure tudna = compensation claim. Consumer court mein jaao — Amitabha Dasgupta case mein SC ne Rs 5 lakh + Rs 1 lakh compensation diya tha aise hi case mein.

Q: Locker rent nahi diya toh kya bank locker tod sakta hai? A: Haan — lekin proper procedure ke saath. Generally 3 saal tak rent default ke baad, multiple notices dene ke baad, bank locker break kar sakta hai. Lekin notice, witness, inventory mandatory hai. Bina notice tudna illegal hai. Isliye rent time pe pay karo.

Q: Bank locker ke liye nomination kyun zaroori hai? A: Nomination ke bina, locker holder ki death ke baad legal heirs ko succession certificate ya legal heir certificate chahiye locker access ke liye — yeh mahino lag sakta hai. Nomination registered ho toh nominee directly access kar sakta hai (proper procedure ke saath). Bank locker ke rules ke under nomination facility available hai — zaroor use karo. bank locker ke rules

Q: Kya bank ko pata hota hai locker mein kya hai? A: Nahi — bank ko locker contents ka pata nahi hota (privacy). Lekin Supreme Court ne Amitabha Dasgupta case mein clearly kaha — “contents nahi jaante” yeh excuse bank ko liability se exempt nahi karta. Bank ko locker system aur security maintain karni hai — chahe contents kuch bhi hon. Negligence pe liable rahega. bank locker ke rules

Q: Bank locker ke rules ke under bank ke against complaint kahan karein? A: 4-step escalation — (1) Bank branch manager ko written complaint; (2) Bank Nodal Officer — internal grievance; (3) RBI Banking Ombudsman — cms.rbi.org.in (free, online); (4) Consumer Court — District Commission (deficiency of service). Amitabha Dasgupta judgment ne confirm kiya ki locker disputes consumer court ke under aate hain.

Locker Safe Hai — Lekin Apni Suraksha Khud Karo

Bank locker ke rules ke baare mein sach yeh hai — bank locker safe hai, lekin bank aapke contents ka insurer nahi hai. RBI 2021 rules aur Amitabha Dasgupta Supreme Court judgment ne clear kar diya — bank ki liability limited hai (100x rent), aur sirf negligence cases mein.

Isliye smart approach yeh hai — locker use karo, lekin high-value items ka separate insurance lo. Documentation maintain karo. Nomination register karo. Aur apne rights jaano taaki agar kuch ho — toh aap compensation claim kar sako.

Yaad rakhein:

- Bank locker ke rules — bank ki liability limited hai, 100% nahi

- 100x annual rent — maximum compensation (negligence cases mein)

- Bank LIABLE — theft, robbery, fire, building collapse, employee fraud

- Bank NOT liable — Act of God (natural disasters), customer’s own negligence

- Amitabha Dasgupta SC (2021) — bank “no liability” claim nahi kar sakta

- Contents insured nahi — separate jewellery/valuables insurance lo

- Nomination register karo — death ke baad family access ke liye

- Break-open procedure — notice + witness + inventory mandatory

- Compensation — bank → ombudsman → consumer court

- Documentation — contents list, purchase bills maintain karo

DuoCounsel ke podcast pe humne banking rights, consumer protection aur financial legal matters pe detailed episodes kiye hain. Zaroor sunein. Agar aapka bank locker se related koi dispute hai ya guidance chahiye — comment mein likhein. Hum practicing advocates hain Gurugram mein aur Punjab & Haryana Bar Council se enrolled hain.

===== AUTHOR SECTION =====

Is Article Ke Baare Mein

Yeh article DuoCounsel ke dono practicing advocates ne banking aur consumer law experience ke aadhar pe likha hai. Bank locker disputes, banking ombudsman matters, consumer commission cases — Adv. Yogesh Solanki aur Adv. Barkha Jain handle karte hain.

👨⚖️ Adv. Yogesh Solanki

Co-Founder, DuoCounsel | Punjab & Haryana Bar Council

Adv. Yogesh Solanki DuoCounsel ke Co-Founder aur Punjab & Haryana Bar Council se enrolled practicing advocate hain. Gurugram District Courts mein active practice — RERA disputes, consumer cases, civil litigation, property disputes aur criminal matters mein specialization. Solanki Engineers ke official legal retainer.

Banking disputes, locker liability cases, consumer commission proceedings — Yogesh ka Gurugram District Consumer Commission mein direct experience hai. DuoCounsel podcast ke through legal awareness Hinglish mein pahunchate hain.

Specialization: Consumer Law | Banking Disputes | RERA | Civil Litigation | Property Disputes | Criminal Law | MACT Claims

📍 Practice: Gurugram District Courts | Punjab & Haryana High Court

👩⚖️ Adv. Barkha Jain

Co-Founder, DuoCounsel | Punjab & Haryana Bar Council

Adv. Barkha Jain DuoCounsel ki Co-Founder aur Punjab & Haryana Bar Council se enrolled practicing advocate hain. Corporate law, business compliance, banking regulations aur consumer protection mein deep expertise.

Banking compliance, locker agreements, RBI guidelines interpretation, financial disputes — Barkha ka corporate aur banking context mein extensive experience hai. DuoCounsel podcast mein complex matters simple Hinglish mein explain karti hain.

Specialization: Corporate Law | Banking Law | Consumer Protection | Business Compliance | GST | Income Tax | Matrimonial Law

📍 Practice: Gurugram District Courts | Punjab & Haryana High Court

⚠️ Disclaimer: Yeh article sirf legal awareness aur educational purpose ke liye hai. Bank locker disputes specific facts pe depend karte hain — apne specific situation ke liye qualified advocate se consult karein.

🎙️ DuoCounsel Podcast sunein — legal awareness Hinglish mein | duocounsel.com/podcast